The U.S. Congress is once more on the verge of a potential government shutdown, adding to the nation’s economic woes. If an agreement on federal funding isn’t reached, the government may have to implement furloughs and halt certain payments from October 1st. The House Republicans are divided over the spending cuts to propose, with some aiming to undermine a bipartisan agreement from earlier this year.

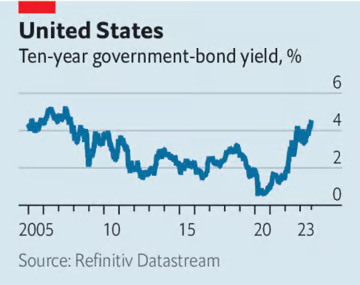

However, the real economic concern for the U.S. isn’t this potential shutdown but the broader budgetary issues, which are deteriorating monthly. The real alarm bells are ringing in the bond markets. The cost for the U.S. government to borrow for a decade has surged to its highest since 2007, at 4.6%. While bond yields have been on the rise, the federal government’s debt ratio has almost tripled, making rising interest rates more burdensome.

Consequently, the government’s debt service costs are projected to double in a decade, reaching an all-time high by 2030. This projection might even be optimistic, as it doesn’t account for the recent bond market shifts. If current rates persist, by 2051, debt interest could eat up nearly half of federal tax revenues unless there are significant tax hikes or spending cuts.

The U.S. deficit has soared over the past year under the Biden administration, explaining the anticipation of persistently high interest rates. This deficit is pushing up interest rates, which in turn affects inflation and the Federal Reserve’s rate decisions. The U.S. deficit is also a reason why its economy remains resilient despite tighter monetary policies and why its bond yields have surpassed those in the euro zone.

With the U.S. government’s continued borrowing spree, expecting a significant drop in interest rates seems unrealistic. The fiscal policy appears set to remain unchecked. While some fiscal tightening is on the horizon, it’s primarily due to a Supreme Court decision. The real long-term budgetary strain comes from mandatory spending increases, which no one seems ready to address. The looming decision on whether to extend Trump’s 2017 tax cuts, set to expire in 2025, adds another layer of complexity.

Currently, the rise in U.S. bond yields is primarily due to anticipated interest rate hikes, not prolonged inflation or default fears. However, if politicians continue to ignore rising deficits and borrowing costs, they might soon face a tough decision between long-term austerity measures and influencing the Federal Reserve’s monetary policy decisions. This could trigger more inflation and destabilize the economy, making the current shutdown concerns seem minor in comparison.